Factors Affecting Volatility of Silver Prices

Faculty Contributor : A. Damodaran, Professor

Student Contributors : Abhishek Aggrawal and Aditya Bhargava

The price of silver has been very volatile historically. Although the ratio of gold to silver prices has varied over the past, in recent times we observe that silver prices follow gold prices and may act as a substitute for them in the future. This article tries to identify the major factors that cause volatility in the silver prices and analyse in detail the impact of these factors on the silver prices. The study aims to provide directional inputs that can help predict future trends in the silver prices.

Silver is one of the most precious metals, valued both as a form of currency and store of value. The major components of silver demand1 are Industrial use (54%), Photography (15%), Jewellery and Silverware (26%) and Coins (5%). Twenty countries together produce 96% of the silver mined globally2. Mexico is the largest producer followed closely by Peru3. The main consumer countries for silver are the US, India, Canada, Mexico, UK, France, Germany, Italy and Japan.

The key factors that affect the volatility of silver are fluctuating industrial demand and store of value demand, geo-political uncertainties, rising crude oil prices, depreciating dollar, government policies on major export and import destinations, sales by China and other central banks, direction of gold prices and direction of other commodity prices.

Analysis of Silver Price Movement

The analysis is based on the past 5 year Silver US prices and Silver MCX prices data. The pre-recession and post-recession periods have been treated independently.

Spot

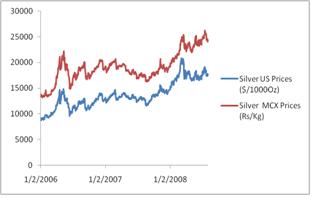

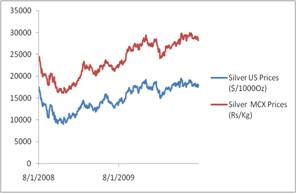

We begin our analysis from the year 2006 (Exhibit 1). The year saw silver outpacing its other commodity counterparts-gold and platinum, growing at a rate of 58% during the year. Much of this demand is attributable to the launch of Silver Exchange Traded Funds (ETFs) by Barclays. The upward trend continued in 2007 with an increase in the investorsÆ appetite for silver and strong industrial demand. The end of 2008 (Exhibit 2) saw the US experiencing the subprime crisis. This affected the economic outlook and the world economies in an extremely negative manner. Silver and other commodities saw a steep drop in prices as the investors looked for safer havens. This drop was much more for silver than what gold and platinum experienced. Early 2009 saw signs of recovery for silver. Much of 2009Æs strength in investment is attributable to soaring demand for Silver ETFs as well as physical retail investment.

Exhibit 1 Silver Prices Pre-Recession

Exhibit 1 Silver Prices Pre-Recession

Exhibit 2 Silver Prices Post-Recession

Exhibit 2 Silver Prices Post-Recession

Futures

Pre-recession silver had been following an upward trend. Also the basis had been positive which showed that the future remained in normal contango (in an ideal scenario the futures price must be higher than the spot price, hence having a positive basis. This condition is called contango). This clearly indicates that pre-recession there was good supply for silver. Post-recession we see that the demand for precious metals and other commodities went down. The mining of metals for which silver has been a by-product took a hit. The future also went into normal backwardation during the period September 2008- December 2008. This was due to the weak confidence in the silver future markets. However, the demand for silver in the electronics industry4 helped the metal to rise and get the futures back into a contango state.

Basis

Silver has mostly been in contango, but recently this basis has started weakening. Also, the 9 month basis has been higher than the 3 month basis. This clearly indicates that the supply in short term has been tight5. The reason that is attributed to tightening is that silver unlike gold is also used as an industrial commodity. Its industrial demand took a huge setback after the fallout. Another reason that has been stated for the low volumes in the silver futures market has been the investigation by the Commodity Futures Trading Commission (CFTC) for market manipulation and price suppression. Based on the above mentioned facts, we can conclude that as long as the demand for other metals does not pick up, creating a surplus production of silver, the basis between spot and futures can be expected to remain small.

Factors Affecting Silver Prices

We have, in our research, tried to identify the most important factors that cause fluctuations in silver prices. We also tried to understand how their change impacts silver prices.

Large and Private Institutional Investors

Other than the most influential impact of the Hunt Brothers, in 1997, Warren Buffett purchased 130 million troy ounces (4,000 metric tons) of silver at approximately $4.50 per troy ounce (total value $585 million). Also, in April 2006, iShares launched a silver exchange-traded fund, called the iShares Silver Trust which as of April 2008 held 180 million Oz silver as reserves6. This clearly indicates that large investors have the power to affect market prices.

Large Concentrated Short Position

CFTC reported that four or fewer largest traders are holding 90% of all short silver contracts7. They were short by 245 million troy ounces (as of April 2007), which is equivalent to 140 days of production.

Industrial Demand

New applications for silver are being explored in batteries, superconductors and microcircuits, which may further increase non-investment demand. The expansion of the middle classes in emerging economies aspiring to Western lifestyles and products may also contribute to a long-term rise in industrial usage. Moreover, retail investorsÆ strong interest in ETFs helps to explain the growth in demand from this group for physical bullion over the rally-to date8.

Gold Prices

Despite all of silverÆs fundamental drivers, gold is considered as the primary driver for silver prices9. In a bullish environment, speculators tend to be interested in most of the precious metals. So it leads to an increase in the investment demand for silver. Silver having a comparatively smaller market as compared to gold, it does not take much time to drive the prices higher. At the same time when the environment is bearish, investors lose confidence in silver very fast and cause the prices to fall. From the analysis of the trend of the gold-silver ratio, it can be seen clearly that silver has a tendency to follow the prices of gold.

During the subprime crisis when the view was bearish we clearly see the trend that during the days when the prices of gold increased silver also increased. However, it would pace the gain of gold at best. During the days when the gold prices decreased we see that the silver prices plummeted by an even greater margin. Based on our hypothesis we would recommend to buy silver during a recession and to sell during a boom.

US Dollar

From our study of the relation between silver and US Dollar we can clearly see that there exists an inverse relationship between silver prices and USD Index. During recession US Dollar is considered a safe haven, people around the world tend to disinvest in commodities and invest into US Dollar. From our analysis, we can clearly see that the prices of precious metals such as silver, palladium, titanium, etc. declines during recessionary periods. The above trend clearly suggests that silver can be used only as a long term hedge against inflation, but it cannot be used in short term as a recessionary hedge.

Oil Prices

Historically oil has shown a strong correlation with gold. Gold and silver also seem to have a stable relationship. Based on this it might be logical to conclude that oil and silver should also have a stable relationship. It has been argued that the mining of silver is an energy intensive process and hence as the oil prices rise or fall, the prices of silver would also rise or fall. This however would be over simplification as it undermines various other important factors. There is also another argument that says that silver and oil should have greater correlation than silver and gold as they are industrial elements and the factors affecting their demands would be common. However, contrary to this silver is not a perishable commodity whereas oil is.

Since the 1960Æs silver and oil have had a 0.7 positive correlation10, this is quite strong but not as strong as of gold and oil that have a correlation of 0.8. Our analysis of the silver and oil relationship shows that silver does have a positive correlation with oil during secular commodities bull periods and the secular bear periods.

Stock Indices

There is certainly some interplay between the fortunes of the stock markets and capital flowing into silver. SilverÆs appeal as an alternative asset is definitely higher when traditional investments are not faring well11. Yet, the relationship between silver and the S&P 500 (SPX) is far more nuanced and complex than merely a direct inverse or even parallel relationship. The SPX is not, and never has been, silverÆs primary driver.

Running regression across top indices such as S&P 500, Dow Jones, BSE and NSE we see a common pattern emerging. The correlation between silver and the stock markets was low pre-recession. But we see that during the subprime crisis and post it, silver has been highly correlated with the stock markets. This shows the returning demand for investment in silver with the growing confidence in the markets.

Regulation in Silver Market

In response to various complaints from investors in recent past, CFTC has closely studied the existing controls in the market to prevent manipulation12. However, there is no evidence of attempted manipulation as claimed by the complainants. The clear outperformance demonstrated by silver prices when compared to other precious metals in the recent years, shows that silver prices are not artificially depressed. The NYMEX price also trades close to the spot price thus showing that close movements are an indicator of healthy market forces in play.

Moreover, there is a slightly positive relationship between the short futures price and spot silver price, which suggests that larger short futures positions are associated with higher prices. However, still many industry experts believe that the silver market is largely controlled by only a few. These investors are suspected to have enough power to corner the market if they wish to.

Conclusion

Silver is a major precious metal, valued as a form of currency and as an industrial metal. It outpaced its other commodity counterparts-gold and platinum, growing at a rate of 58% during 2006. The primary factor that has been attributed to this strong growth is the investment driven demand for silver.

Many consider silver as a future substitute for investment in gold. However its high volatility has still remained a question of interest. The volatility can be attributed to multiple factors like gold and other precious metal prices, major stock market indices, large concentrated short position, US dollar, oil, institutional investors and industrial demand.

Keywords

Finance, Economics and Social Sciences, Commodities, Silver

Contributors

A. Damodaran is a Professor in the Economics and Social Sciences Area at IIM Bangalore. He is also the Chairperson of the Post Graduate Programme in Public Policy and Management. He holds Ph. D. in Economics from University of Kerala. He can be reached at

damodaran@iimb.ernet.in.

Abhishek Aggrawal (PGP 2009-11) holds a B.E. degree in Chemical Engineering from Indian Institute of Technology (IIT), Delhi. He can be reached at

abhishek.aggrawal09@iimb.ernet.in.

Aditya Bhargava (PGP 2009-11) holds a B.Tech degree in Computer Science and Engineering from Visvesvaraya National Institute of Technology (VNIT), Nagpur. He can be reached at

aditya.bhargava09@iimb.ernet.in

References

-

Reliance Money Research, 2009, ōReport on Silverö, http://www.reliancemoney.com/cmt/upload/research/PN_SILVER.pdf. Last accessed on June 18, 2011

-

Philip Klapwij, GFMS Ltd, May 2008, ōWorld Silver Survey 2008ö, The Silver Institute Presentation,

http://www.gfms.co.uk/Market%20Commentary/GFMS_WSS_2008_Presentation.pdf. Last accessed on June 18, 2011

-

Top 20 Silver Producing countries in 2010, 2011, "Silver Production 2010", The Silver Institute Website,

http://www.silverinstitute.org/production.php. Last accessed on June 18, 2011

-

Uses of Silver, Electrical & Electronics, 2011, "The online guide top bullion investing",

http://www.ebullionguide.com/silver.aspx. Last accessed on June 18, 2011

-

Jake Towne, 2009, "Silver in Backwardation! Has the Last Contango Been Danced in Washington?",

http://www.nolanchart.com/article5916.html. Last accessed on June 18, 2011

-

Resource Intelligence Website, 2009, "Silver Prices & Information on Silver Investing",

http://www.resourceintelligence.net/silver-prices-information-on-gold-investing/3475. Last accessed on June 18, 2011

-

Commodity Futures Trading Commission, 2008, "Report on Large Short Trader Activity in the Silver Futures Market",

http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/silverfuturesmarketreport0508.pdf. Last accessed on June 18, 2011

-

Silver Institute, May 2009, "Silver Investment Market Report 2009",

http://irametals.com/Silver%20Institute%20Investment%20Mkt%20Report%204.2009.pdf. Last accessed on June 18, 2011

-

Adam Hamilton, Zeal Intelligence LLC, 2010, "Silver/Gold Ratio Reversion 4", Silver Seek website,

http://news.silverseek.com/Zealllc/1292606323.php. Last accessed on June 18, 2011

-

Adam Hamilton, 2005, "Silver/Oil Ratio Extremes", Zeal LLC website,

http://www.zealllc.com/2005/sor.htm. Last accessed on June 18, 2011

-

Adam Hamilton, March 2009, "Gold and the SPX",

http://www.safehaven.com/print/12819/gold-and-the-spx. Last accessed on August 18,2010

-

Commodity Futures Trading Commission, 2008, "Report on Large Short Trader Activity in the Silver Futures Market

http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/silverfuturesmarketreport0508.pdf. Last accessed on June 18, 2011